Marketing+Finance

UCSD MGT 100 Week 10

Let’s reflect

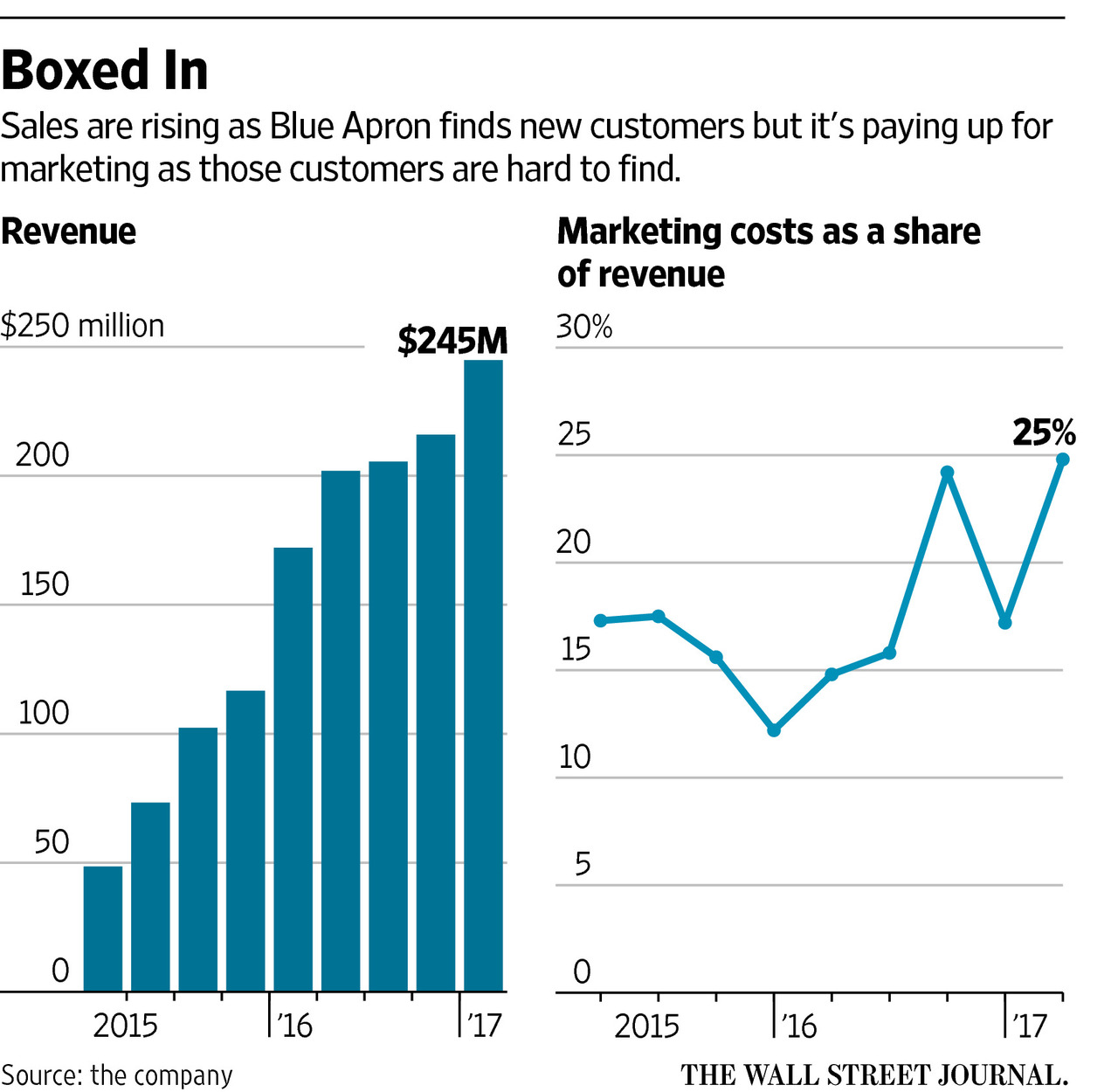

Blue Apron in 2017

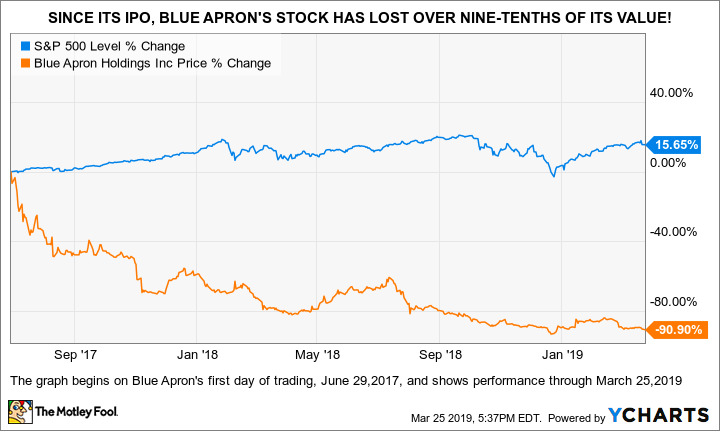

Blue Apron in 2019

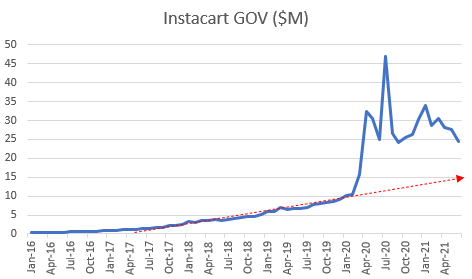

Instacart Gross Order Value

![]()

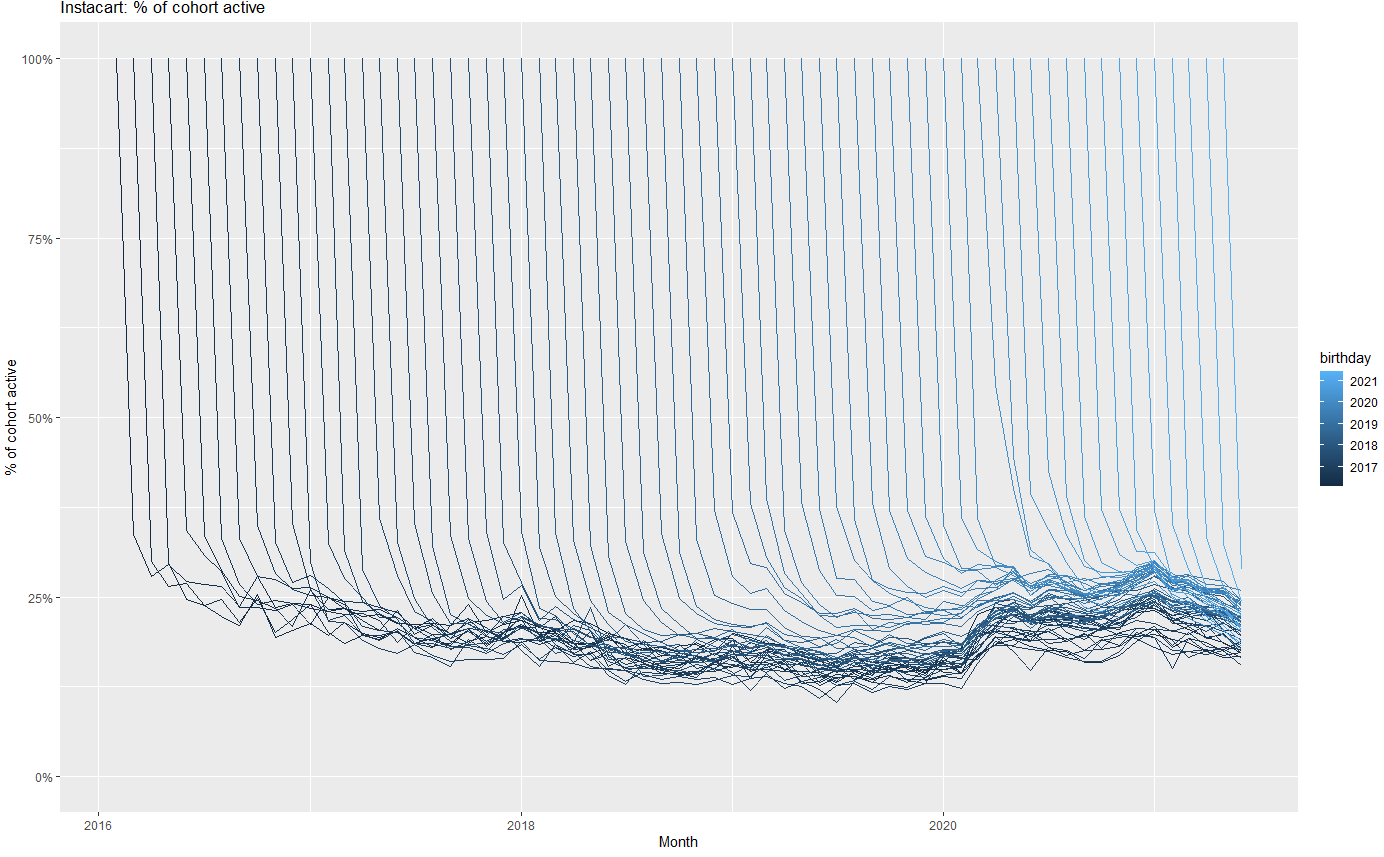

Instacart Retention by Cohort

![]()

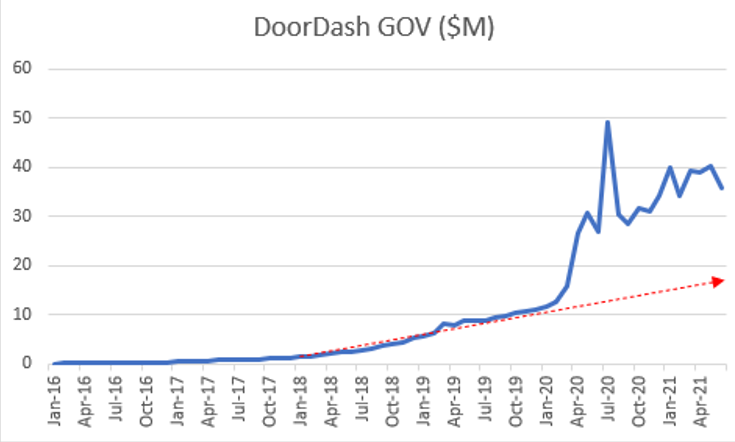

Doordash Gross Order Value

![]()

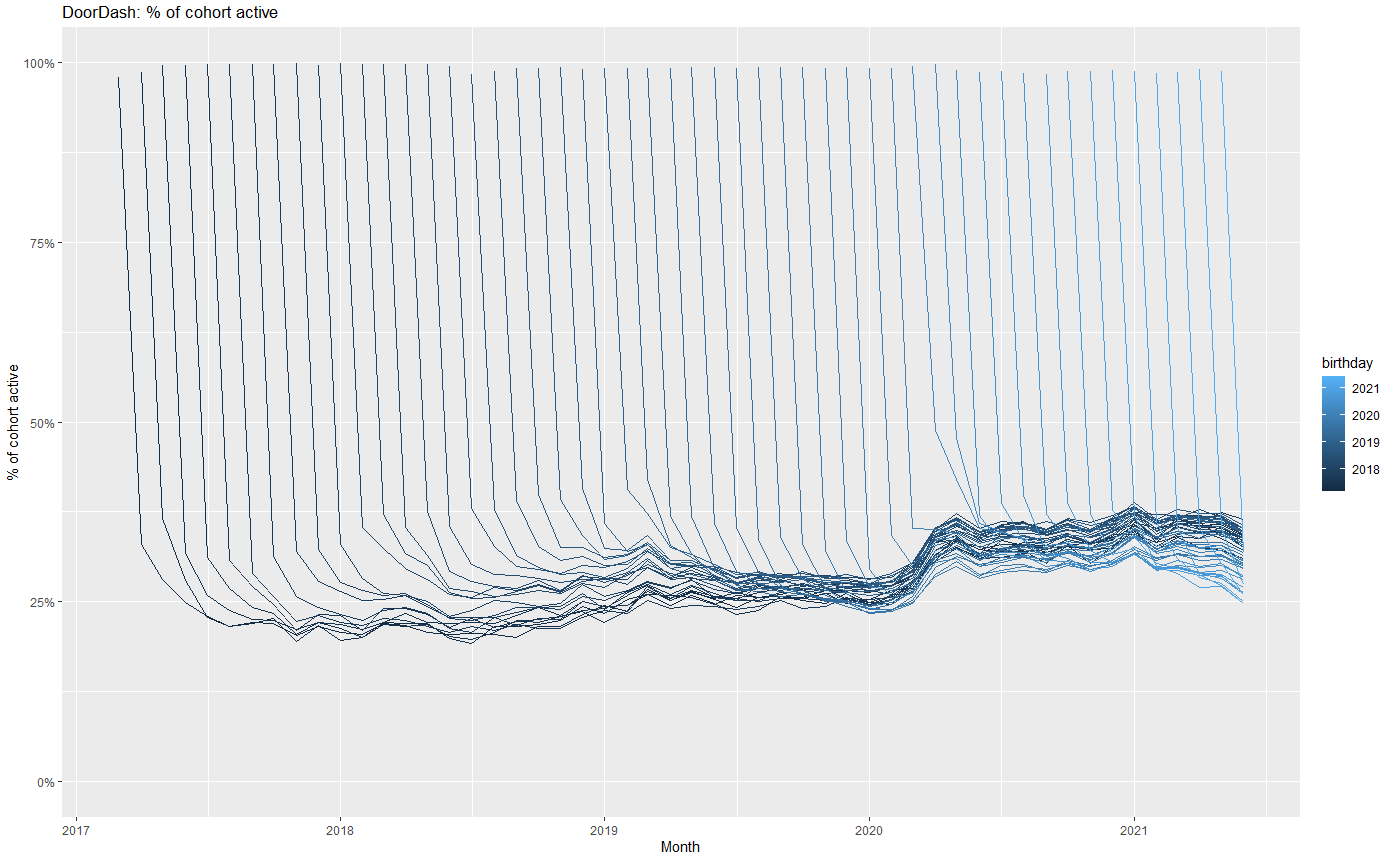

Doordash Retention by Cohort

![]()

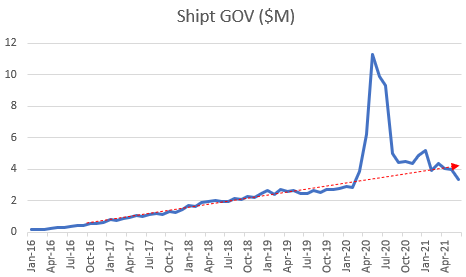

Shipt Gross Order Value

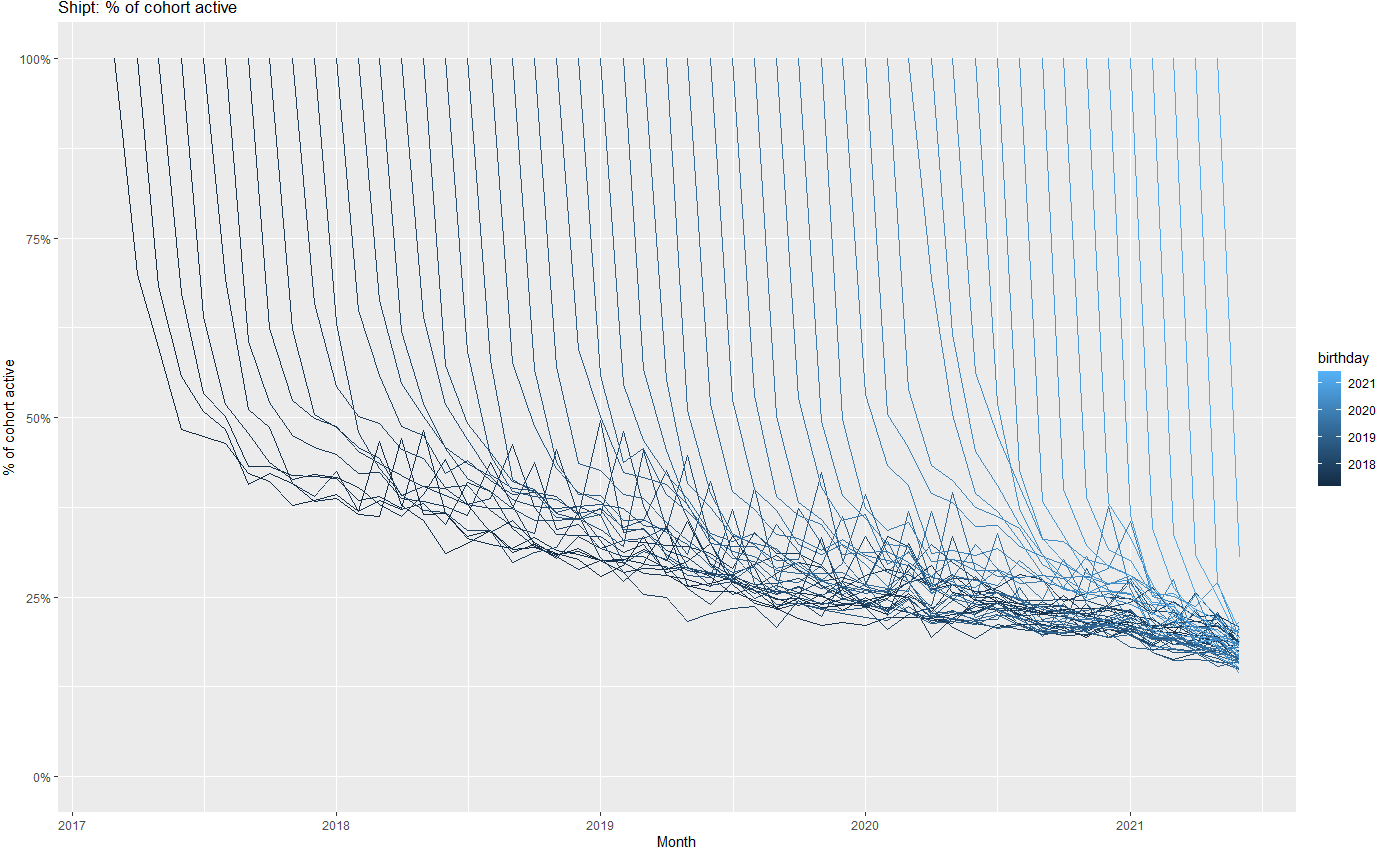

Shipt Retention by Cohort

Let’s play!

Homework

No assignment or quiz

Chat briefly about the final

Congrats you did it!

Special congratulations for those who are graduating

- It's a big deal. We're proud of you.

Recap

- Corporate valuation uses past profits to predict future profits, without using granular customer metrics

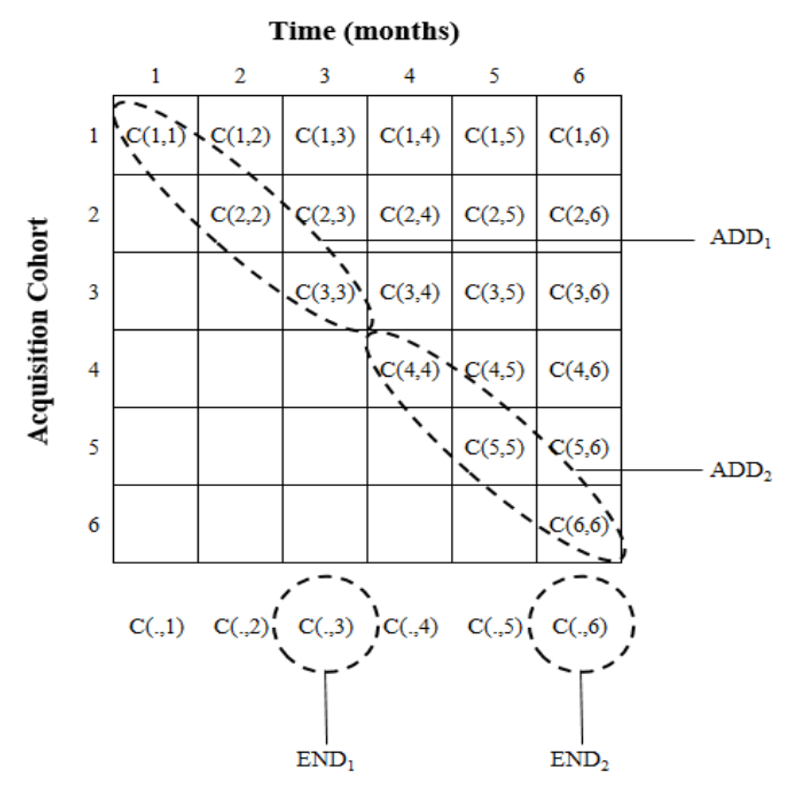

- Customer-Based Corporate Valuation (CBCV) advocates reporting \(C(t,t')\) to enable investors to better predict profits

- CBCV is still small but growing, there are opportunities here

- Fundamentals help calculate asset prices

- No customers, no business

Going further

What are the most important statistical ideas of the past 50 years?

Customer-Based Corporate Valuation for Publicly Traded Noncontractual Firms

Decomposing Firm Value by Belo et al. (2021) for a competing perspective