Demand Modeling

MGT 100 Week 3

This version: May 2026 | License: CC BY 4.0 | We use javascript to track readership.

We welcome reuse with attribution. Please share widely.

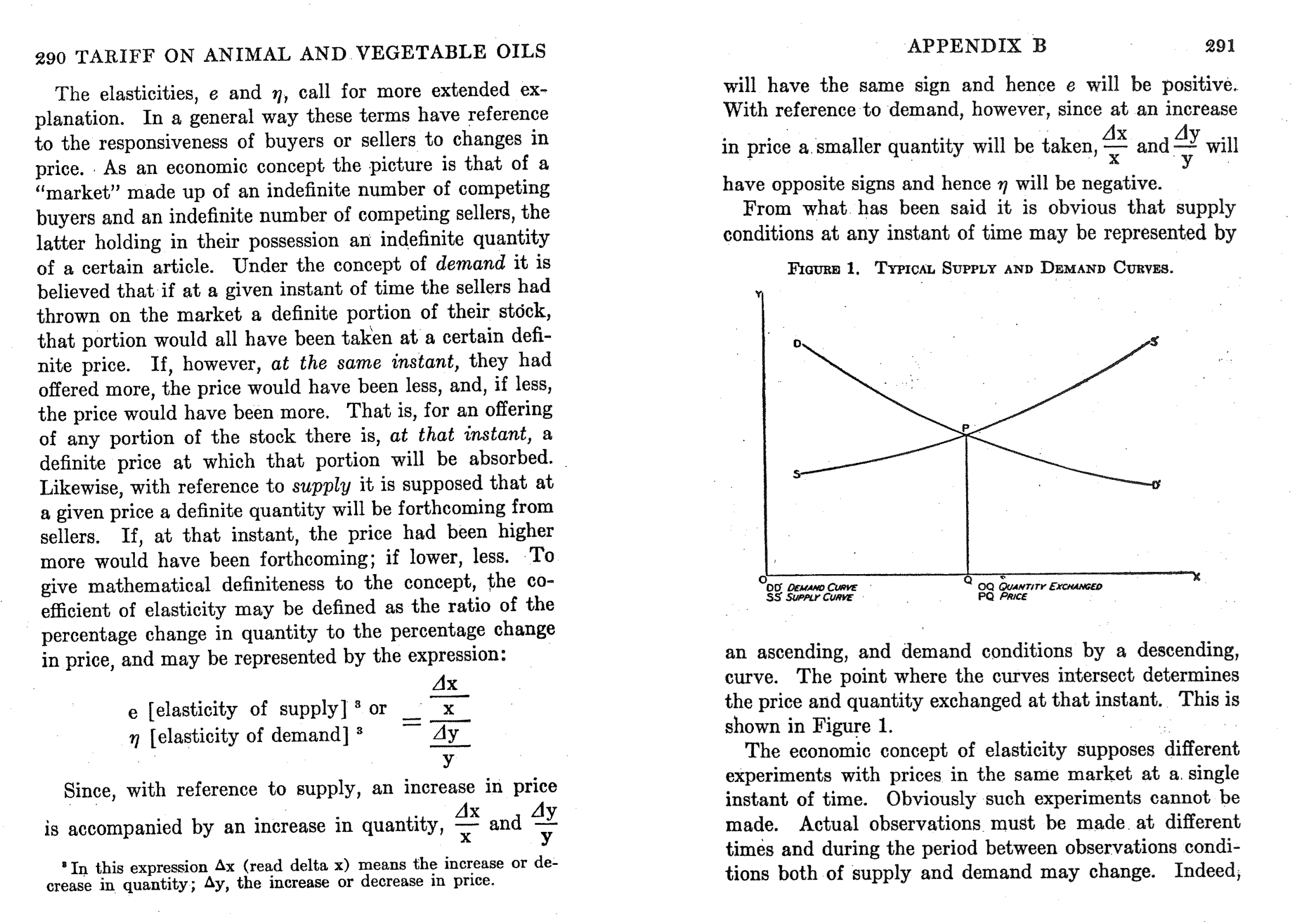

Demand Curve

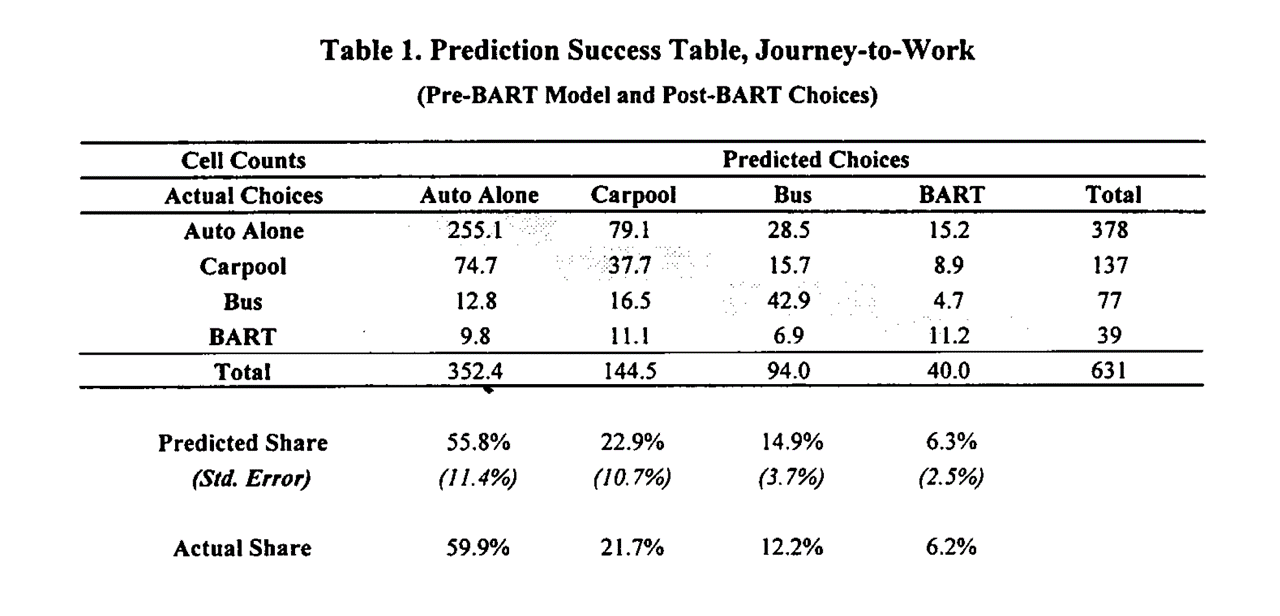

Daniel McFadden & BART

- Economist working at UC Berkeley to empiricize theoretical models of individual choice

- In the early 1970s, funded by NSF to predict how BART would change transit in San Francisco

- Collected pre-BART transportation choices by surveying commuters in neighborhoods slated for BART stations

- Product attributes: walking distance, waiting time, financial cost, automotive preference

- Estimated MNL on pre-BART survey data, then predicted post-BART transit choices

Multinomial Logit (MNL)

IIA: Deeper dive

- Famous example from McFadden (1974): Suppose you estimate demand for transportation with three options: {Blue Bus, Red Bus, Car}, each with 33% market share, and you include product intercepts in utility

- Now suppose you evaluate a counterfactual in which you paint all of the red buses blue, and then you predict market shares in the new choice set {Blue Bus, Car}

- MNL will predict Blue Bus and Car shares of 50%, not 67% and 33%

- Why? MNL infers \(V_{jt}\) based on market shares, so equal market shares imply equal \(V_{jt}\)

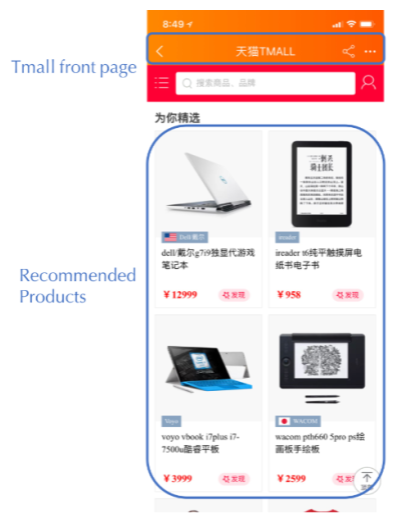

MNL in Practice: Alibaba

- Alibaba recommends 6 personalized products, chosen from thousands, on homepage to maximize sales revenue

- Previously: ML algorithm predicted each product’s purchase probability independently, then displayed the 6 with highest expected revenue

- Feldman et al. (2022) proposed using MNL instead, because MNL captures substitution across products — if two displayed products are similar, they cannibalize each other’s demand rather than generating new sales

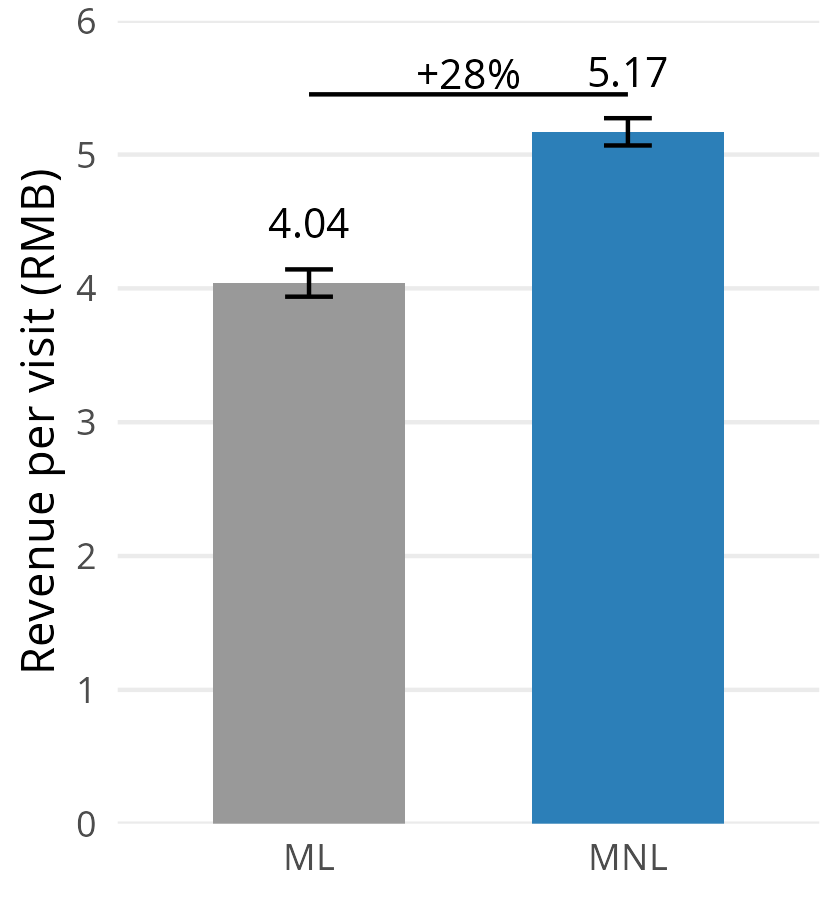

- Field experiment with 5M+ customers on Tmall/Taobao: ML predicted purchase probabilities more accurately, but MNL generated 28% more revenue per visit

- Why? ML ignores substitution and may waste display slots on similar products. MNL’s \(s_{jt}\) formula links all products through the denominator, so it selects more diverse assortments

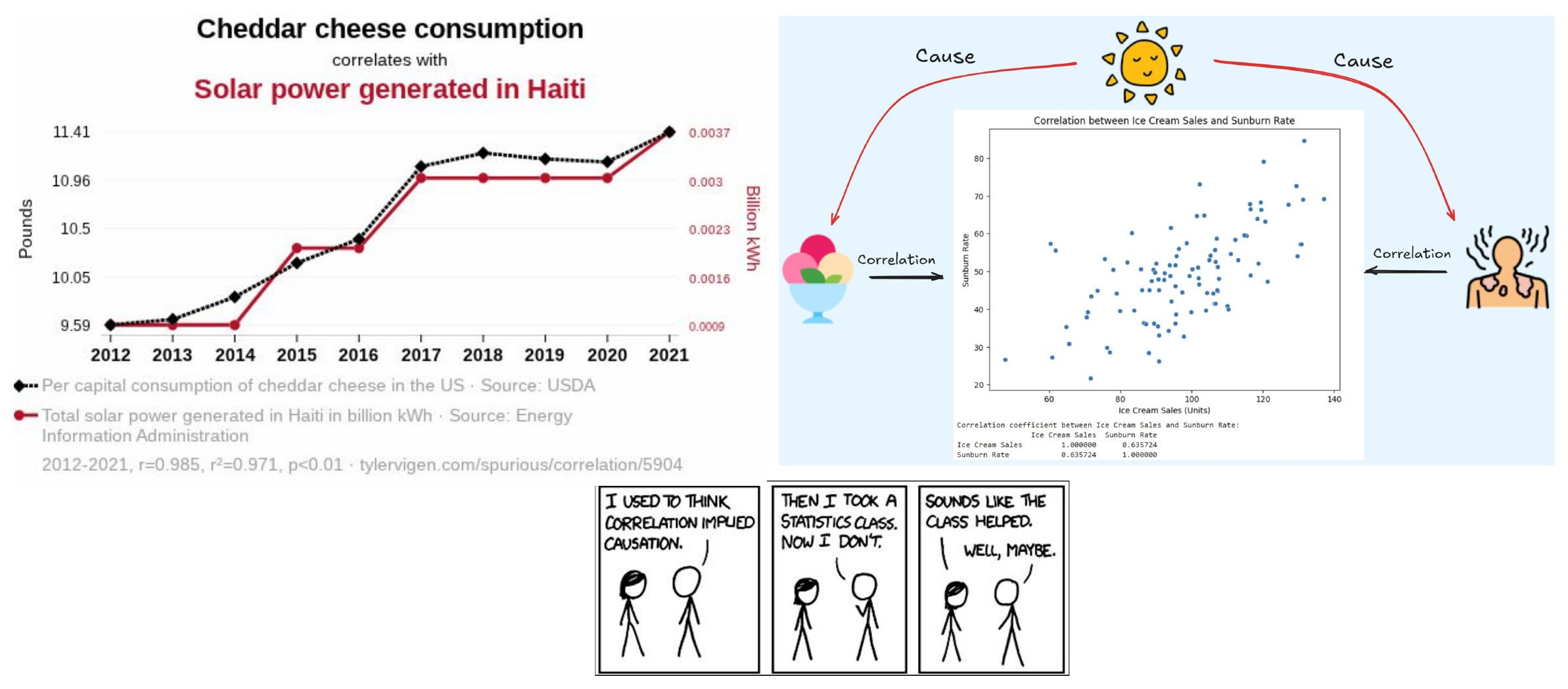

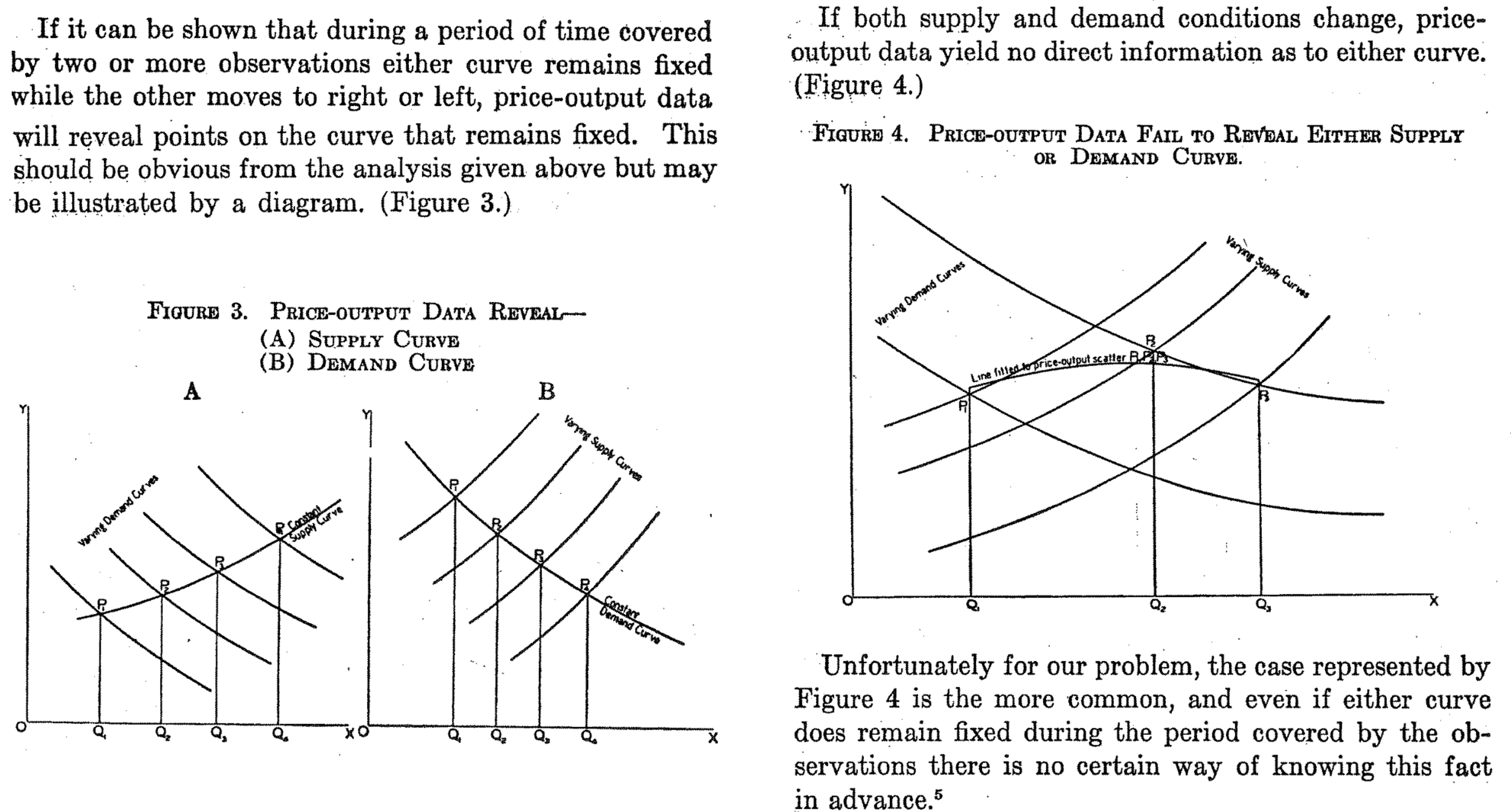

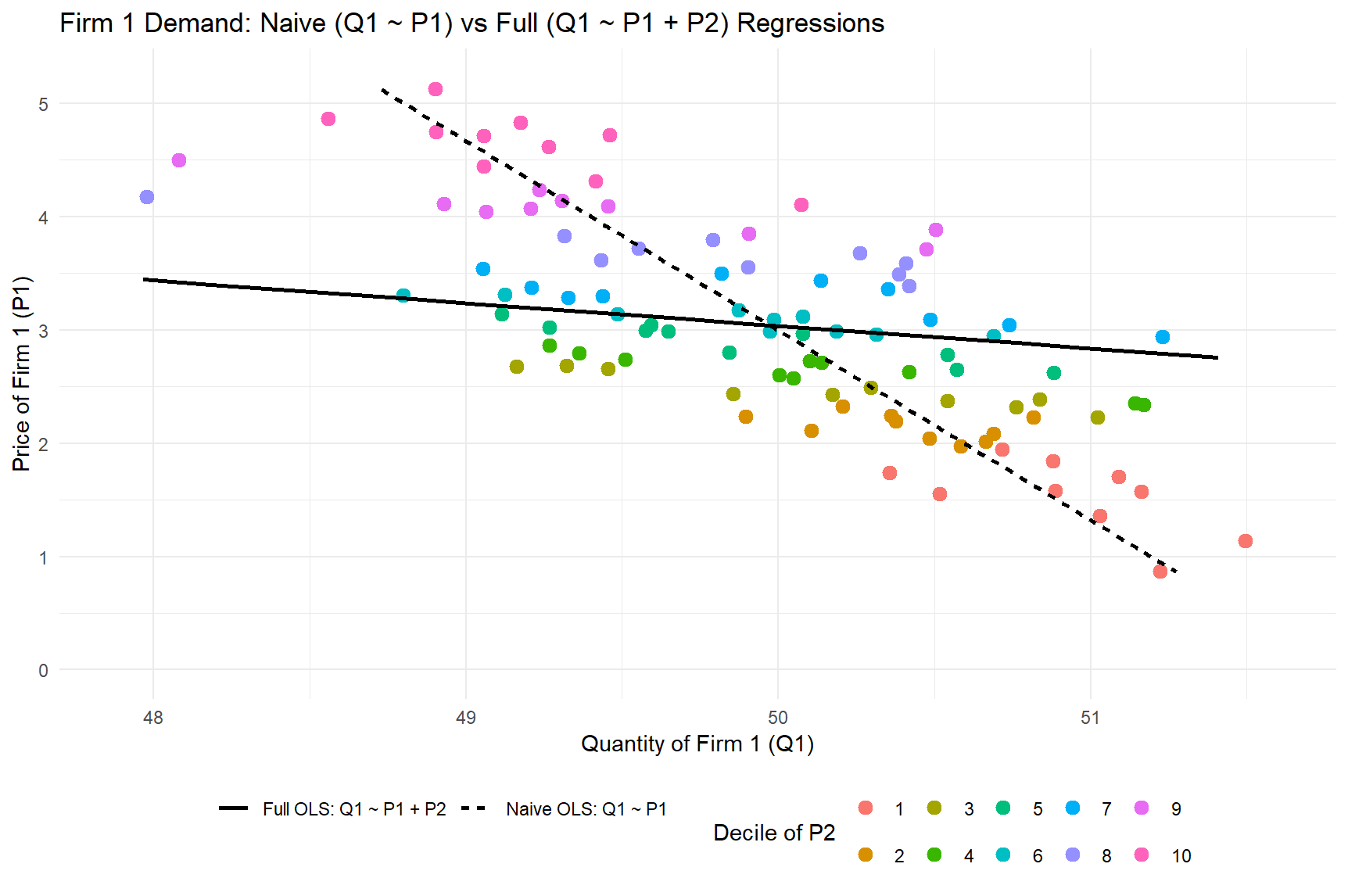

Classic Identification Argument

4. An Analogy

- Foot size significantly predicts reading comprehension among children!

- In fact, age causes foot size and age causes reading comprehension

- Also, crib purchases significantly predict childbirth!

5. Sports example

- Suppose you observe daily sports team ticket prices and sales before and after the team acquires a very popular player

- Prices and sales are both higher after the trade

- Does this mean that higher price caused higher sales?

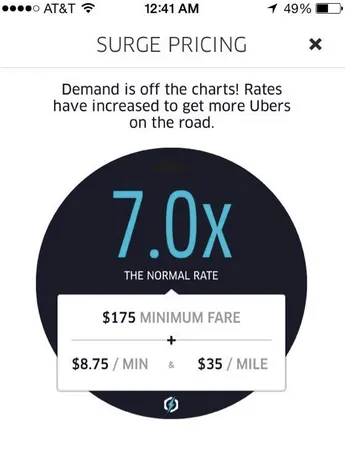

6. Example: Digital systems

- Uber surge pricing:

Positive Demand shocks increase price

Negative Supply shocks increase price - System adjusts the price without knowing the causes

- Many digital inventory-based pricing systems are similar

7. Shrinkflation

- Shrink the package, maintain the price

- Also, “Skimpflation” : reduce ingredient intensity

- Describe price endogeneity in your own words

- Generate a novel example related to price and demand

- If time, explain how you might resolve it

Class script

- Wrangle data

- Estimate MNL

- Interpret parameters and SEs

- Assess model fit

Competition

- Estimate MNL with phone dummies and price on each of the 3 cohorts separately

- Create a visualization showing how the price sensitivity parameter has changed across the 3 years

Recap

- Demand modeling enables data-driven sales predictions for counterfactual prices and attributes, facilitating profit maximization

- MNL is popular bc it is powerful, microfounded and tractable

- MNL has limitations (eg, IIA), but is extensible by modeling heterogeneity

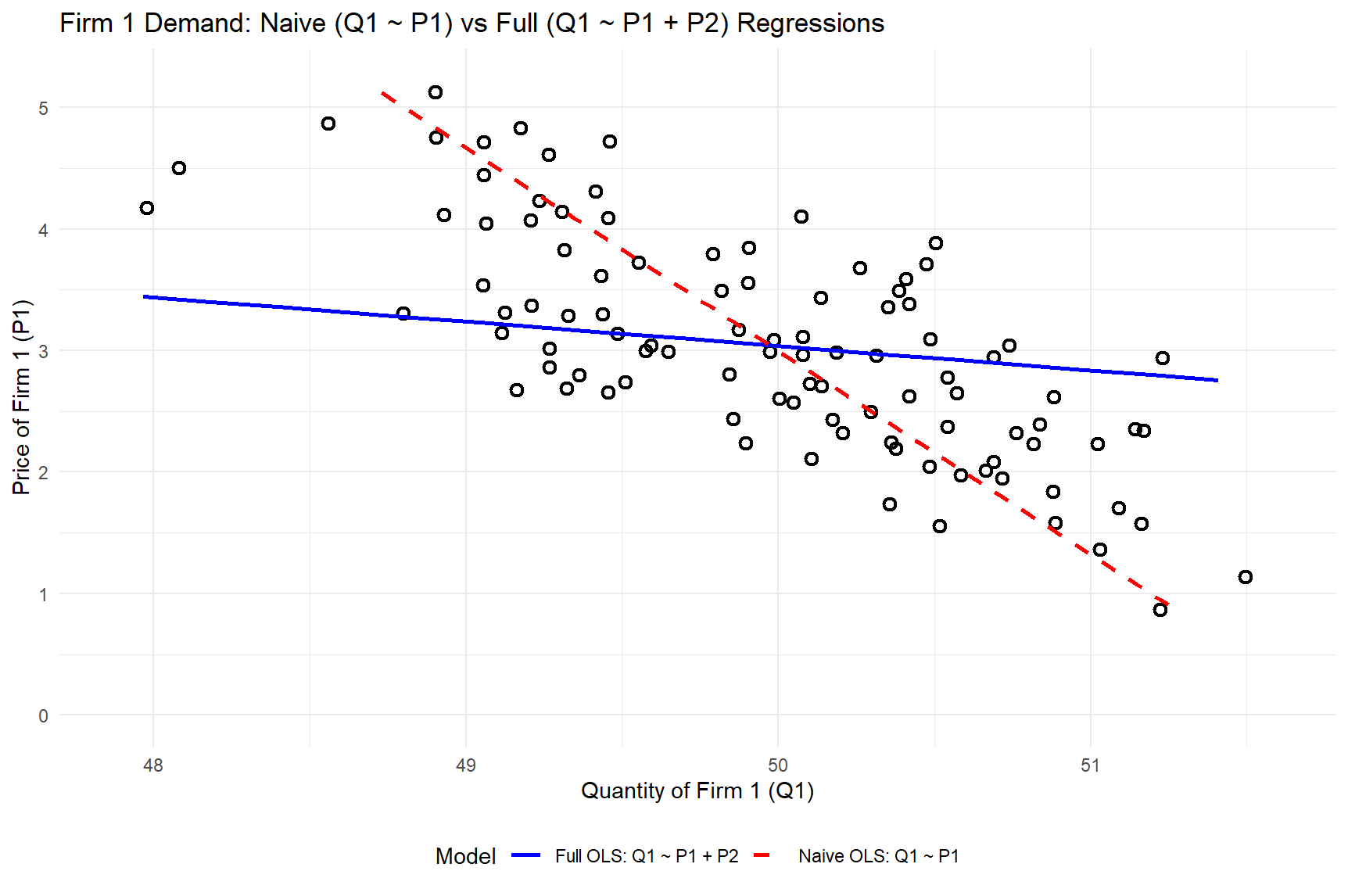

- Price endogeneity is a “data problem” that biases demand parameter estimates when price is correlated with unobserved demand shifters. Usually resolved with exogenous price variation

Going further

- Supply, Demand, and the Instrumental Variable: Lessons for Data Scientists from the Economist’s Toolbox

- Causal inference in economics and marketing (Varian 2016)

- Discrete Choice Analysis with R

- Microeconometric models of consumer demand by Dube (2018)

- Empirical Models of Demand and Supply in Differentiated Products Industries by Gandhi & Nevo