Customers+Finance

UCSD MGT 100 Week 10

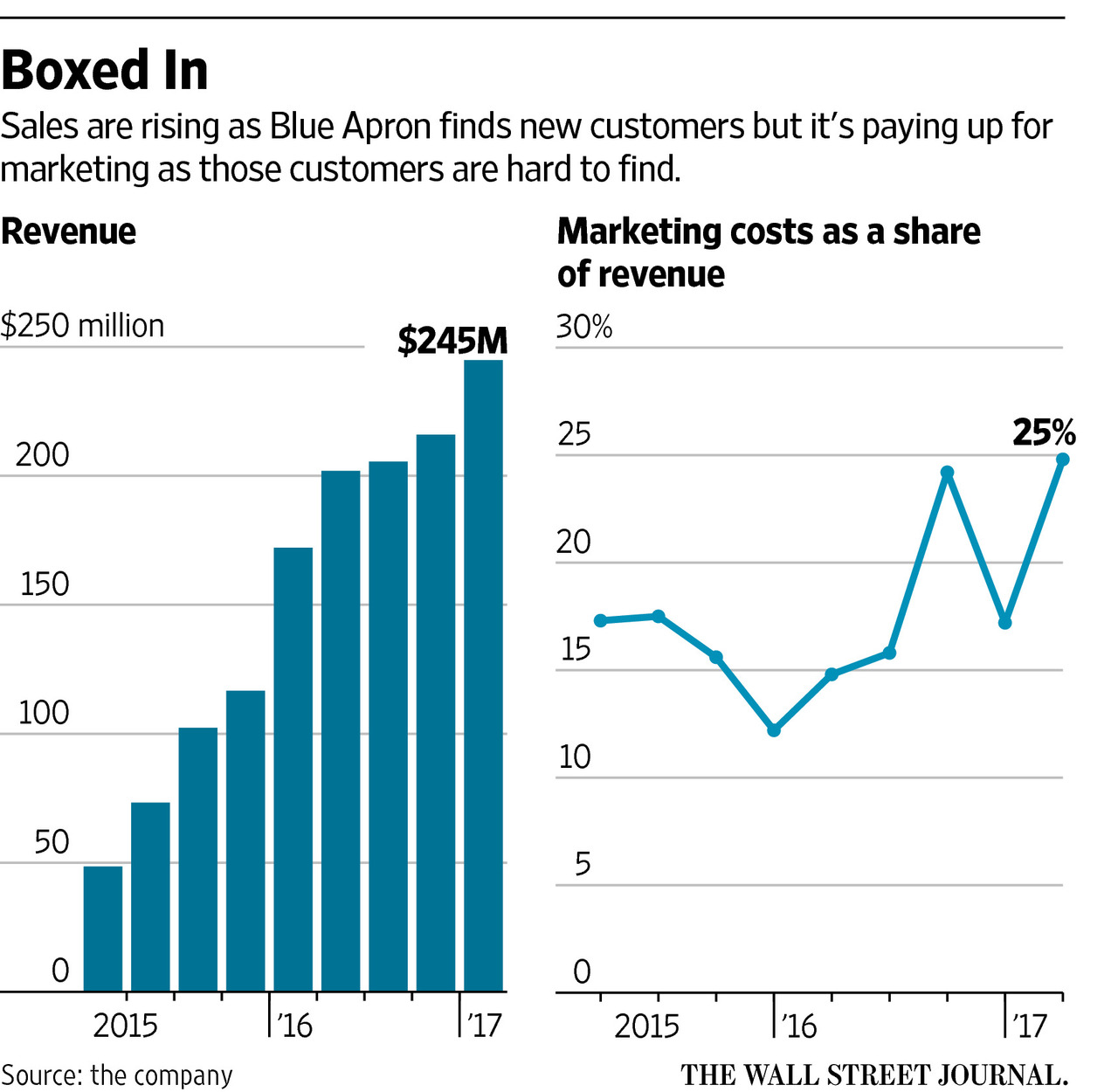

Blue Apron in 2017

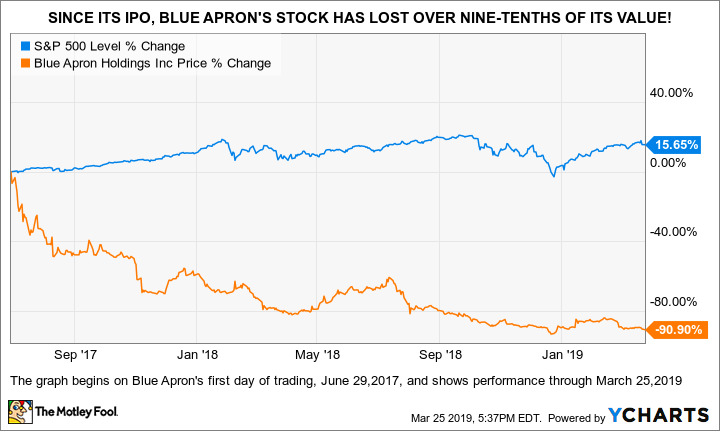

Blue Apron in 2019

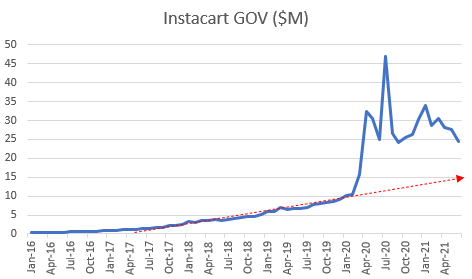

Instacart Gross Order Value

![]()

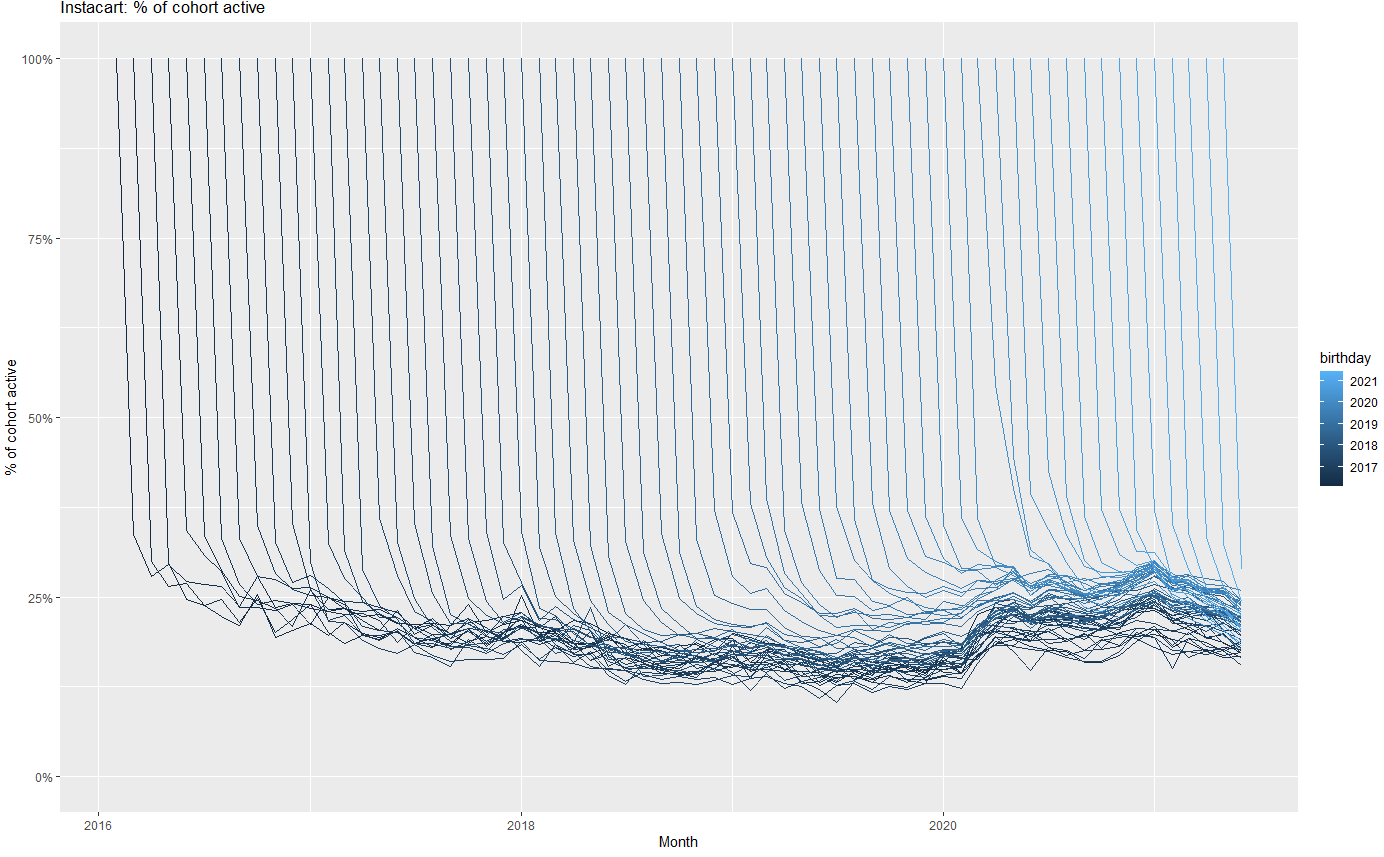

Instacart Retention by Cohort

![]()

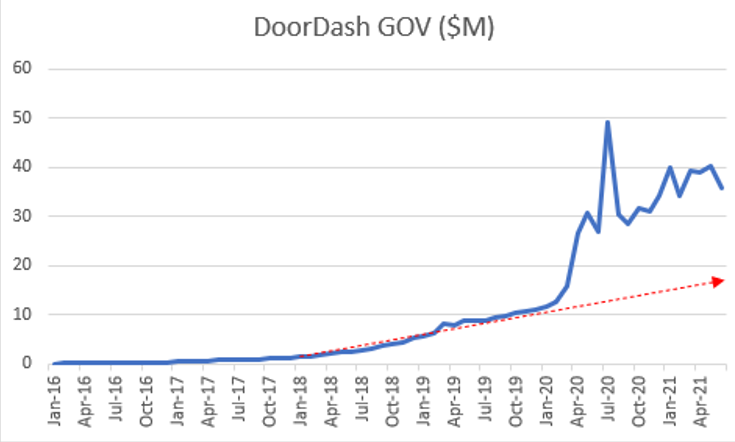

Doordash Gross Order Value

![]()

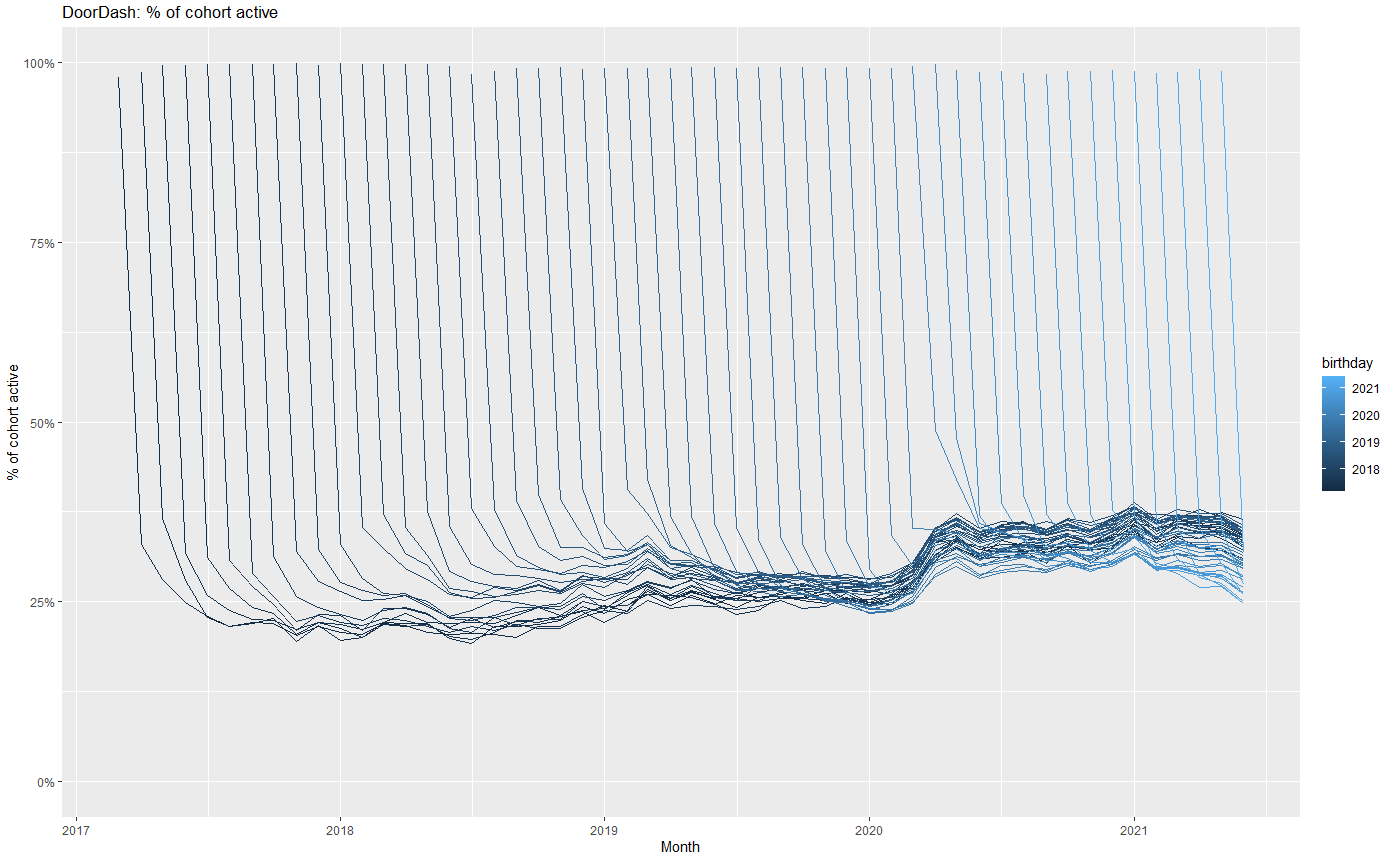

Doordash Retention by Cohort

![]()

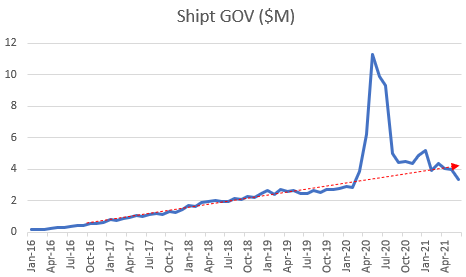

Shipt Gross Order Value

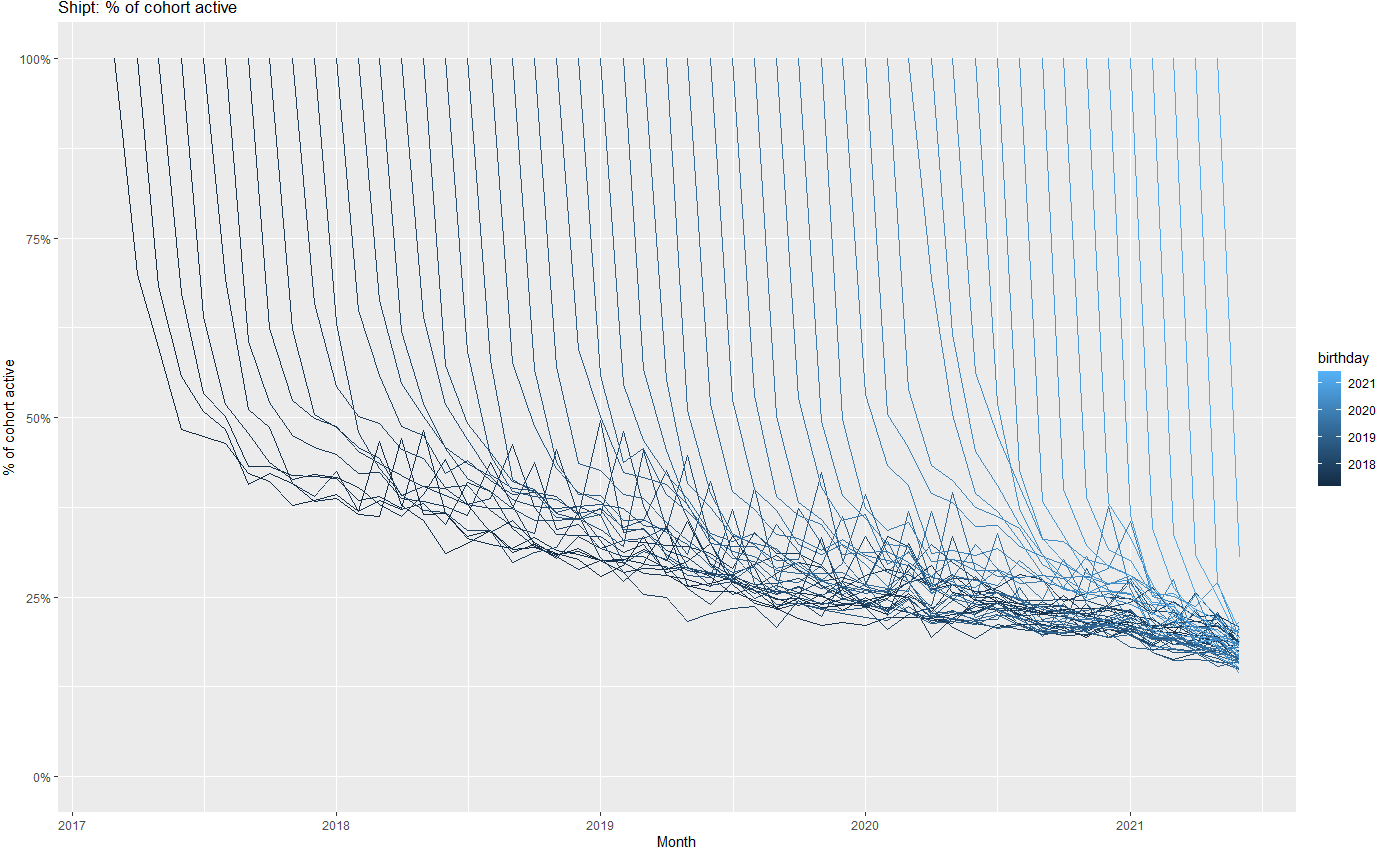

Shipt Retention by Cohort

Let’s play!

Congrats you did it!

Special congratulations for those who are graduating

- It's a big deal. We're proud of you.

Recap

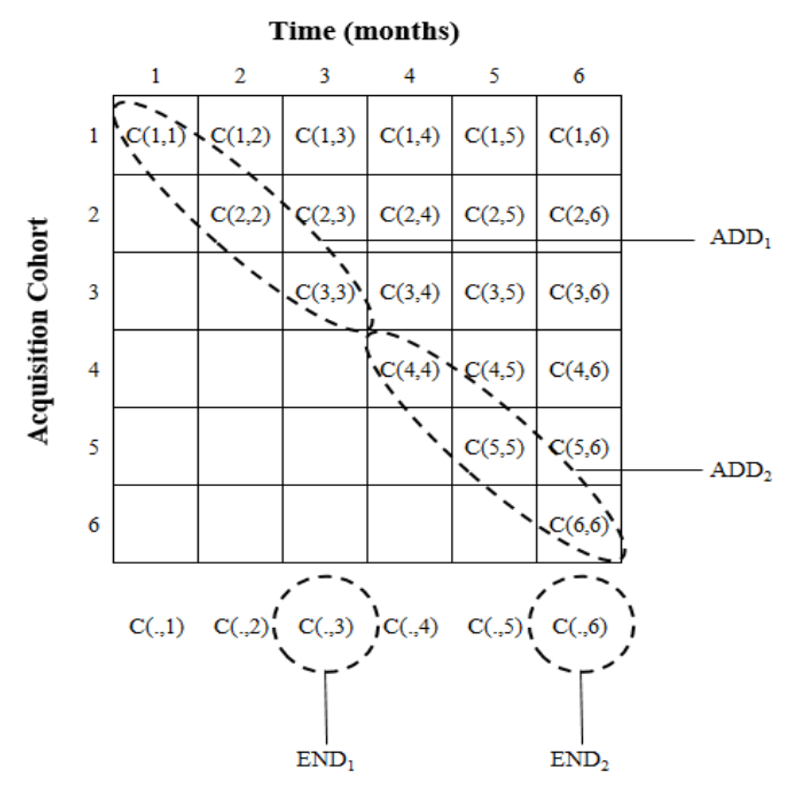

- Corporate valuation uses past profits to predict future profits, without using granular customer metrics

- Customer-Based Corporate Valuation (CBCV) advocates reporting \(C(t,t')\) to enable investors to better predict profits

- CBCV is still small but growing, there are opportunities here

- Fundamentals help calculate asset prices

- No customers, no business

Going further

What are the most important statistical ideas of the past 50 years?

Customer-Based Corporate Valuation for Publicly Traded Noncontractual Firms

Decomposing Firm Value by Belo et al. (2021) for a competing perspective